Can you afford an emergency? UW survey shows many don't have $400 to spare. Blame inflation. | Opinion

With the new year, millions of people resolve to diet, exercise more or make changes in other aspects of their lives, including personal finances. For most of us, personal finance-related resolutions are a combination of spending less, saving more and maybe paying off some debts. Some of the newfound attention to our financial outlook may even stem from an expensive holiday season that just wrapped up. But the new year offers new opportunities to get on track.

Going into 2024, financial resolutions were likely popular across the state. After several years of inflation, finances remain a major concern for Wisconsinites. This comes from a new survey effort at UW-Madison’s Survey Center called "WisconSays," which is a new panel of nearly 4,000 people answering regular survey questions. These data are from the very first wave of that survey.

Polarization isn't a given. The fix? Listen to each other, civil conversations.

We are calling this collaboration the WisconSays/La Follette Survey. These data offer insights into how people are feeling about a range of public policy issues that could be especially important during an election year. Using this information, the La Follette School of Public Affairs and the Milwaukee Journal Sentinel are partnering to share some key findings around critical issues of the day throughout 2024.

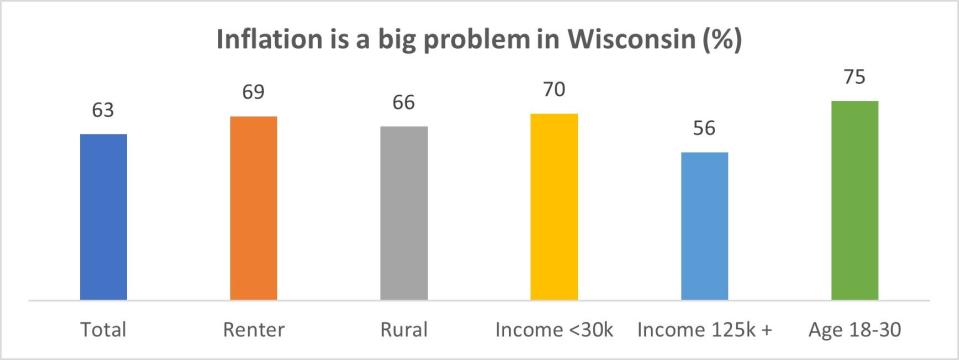

Majority of Wisconsin residents say inflation is big problem

A topic that is always on people’s minds: their pocketbooks. Despite persistent inflation, 2023 was not a bad year economically overall for Wisconsinites. The state’s unemployment rate is low, and wages are rising. But since they are growing at a slower rate than in the US overall, it comes as no surprise that inflation remains a major concern here.

According to the survey panelists, the majority of people (63%) said that inflation was “quite a problem” or an “extremely big problem” in the state of Wisconsin. Renters and people living in rural areas were even more likely to worry about the costs of living, reflecting the added costs they face. It’s hard to make ends meet when you have a low income, but inflation is a challenge everyone faces. While more than two-thirds of people making less than $30,000 think inflation is a big problem, even 56% of people making more than $125,000 said the same.

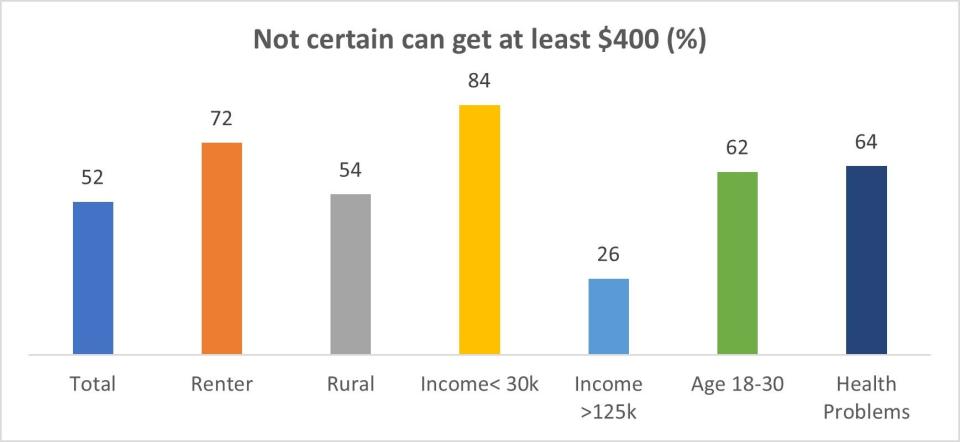

Inflation leaves people with little wiggle room for an unexpected financial emergency — an income shortfall or surprise expense. Indeed, the survey shows that 53% of people in the state are not certain they can find $400 in an emergency. The rate of not having access to money in an emergency is higher among renters (72%), as well as those with lower incomes or health problems. Surprisingly, nearly one-quarter of people making at least $125,000 also lack access to $400 in an emergency.

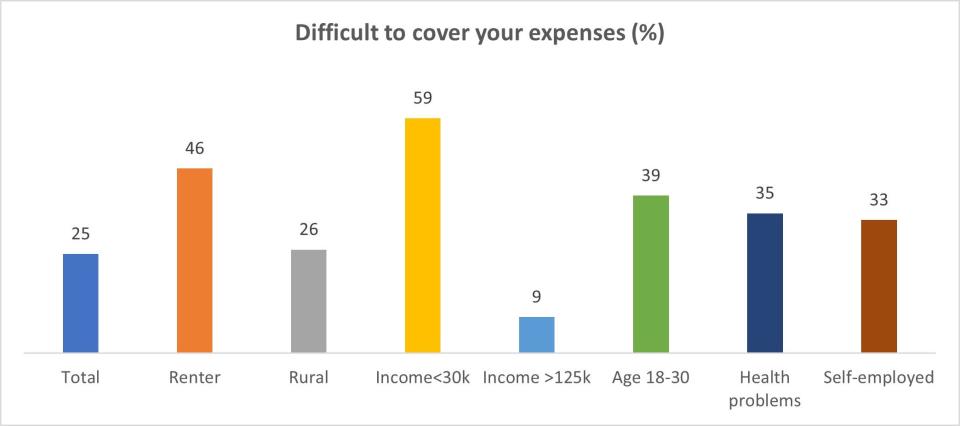

The result of this precarity is that one-in-four Wisconsinites say they are having difficulties paying their basic expenses. The rate among renters is nearly twice as high. Low-income people, people under age 30, those with health problems and the self-employed also are more likely to say they are struggling to get by.

While making ends meet and having an emergency fund are the places to start, saving for the future, including college or retirement are the main priority for most working age people. Many employers across the state have retirement savings options that employees can take advantage of at work, and some will help with emergency and college savings, too.

What we heard listening to voters: Substance and civility matter, the people and their politicians have major disconnects

Access to retirement savings plans at work limited for some

Yet, according to a 2021 FINRA survey, just over half (57%) of people in Wisconsin have access to retirement savings plans at work, although just 41% of people making less than $50,000 do. Expanding access to workplace and individual savings remains an important challenge for our state. At least 16 other states have created retirement savings plans for workers who lack employer-based plans, often combined with automatic enrollment in savings plans. The Wisconsin Legislature is already considering provisions to expand access to college savings at work, which is a welcome step. Other states offer tax credits to small business to set up savings plans, reducing the barriers to offering savings options at work. These efforts will especially benefit young people that the state of Wisconsin needs to retain in the face of an aging population.

Wisconsin Main Street agenda: There is a hunger for thoughtful conversation about pressing policy issues.

Over the last few months, I have been talking with employers, HR directors and employees across the state. Their stories show just how important access to well-designed savings and insurance options at work are for people’s financial security. But their experiences also highlight the tradeoffs between take-home pay and the costs of benefits, especially for people who have lower incomes or work at smaller employers.

The economy in Wisconsin for 2024 is hard to predict, but inflation is not rising as rapidly as it was this time last year, and workers’ incomes are starting to catch up with the cost of living. This presents opportunities for people to re-assess their finances, catch up on bills, prioritize paying down debt, and build up emergency savings. The combination of private sector innovations, new technologies, well-designed employer-based programs, and support from state policies should help Wisconsinites make headway on goals that will improve the financial security of families and communities for years to come. Hopefully future New Year’s resolutions across Wisconsin will focus more on the usual diet and exercise and less on finances.

J. Michael Collins is the Fetzer Family Chair in Consumer and Personal Finance at UW-Madison and a professor in the La Follette School of Public Affairs and the School of Human Ecology. He is a faculty affiliate of the Institute for Research on Poverty and the Center for Demography and Ecology. Collins studies consumer decision-making in the financial marketplace, including the role of public policy in influencing credit, savings and investment choices.

This article originally appeared on Milwaukee Journal Sentinel: How bad is inflation? UW finds most don't have $400 for an emergency